Why FinTechs Rely on Salesforce PAN Authentication Solutions for Customer Onboarding

When a FinTech company loses a customer during onboarding, it rarely announces itself as a compliance failure. It looks like a dropped session, an abandoned form, or a support ticket that never gets resolved. The root cause, more often than not, is identity friction: the gap between what a regulation demands and what a CRM can actually do in real time.

PAN verification sits at the center of this friction for Indian FinTechs, NBFCs, banks, and increasingly, real estate platforms. The problem is not in understanding the need but rather in implementation. Manual checking for the PAN, separate verification through APIs, and lack of process management in Salesforce all contribute to bottlenecks that don’t scale well or sustain under stress.

That’s precisely why enterprise teams are moving toward Salesforce PAN authentication not as a compliance checkbox, but as a structural upgrade to how onboarding works.

The Hidden Cost of Fragmented Identity Verification

Most FinTech teams understand KYC requirements. What they underestimate is the compounding cost of executing those checks outside their CRM.

When verification happens in an external tool or a spreadsheet-based workflow, data must be re-entered, reconciled, and manually linked to the customer record. Each of those steps introduces latency. For a high-volume onboarding pipeline (loans, investment accounts, insurance, or co-lending products), that latency multiplies rapidly.

Beyond speed, there’s a data integrity problem. When PAN verification data doesn’t live inside Salesforce, the audit trail becomes incomplete. Compliance teams are left reconstructing verification history from multiple systems, often during the worst possible moment: an audit or a regulatory query.

The operational argument for Salesforce PAN verification isn’t just efficiency. It’s about closing the loop between the customer record and the compliance record, in one system, in real time.

How Fraud Slips Through Verification Gaps?

Fraudulent identity submissions in financial onboarding have grown more sophisticated. Static PAN entry, where a customer types in a number that passes basic format validation, no longer provides adequate protection. A valid-format PAN may still belong to a deceased individual, a non-existent entity, or a synthetic identity constructed to pass surface-level screening.

Fraud detection PAN Salesforce integration addresses this by moving from format validation to authoritative verification. The distinction matters enormously. Format validation checks whether a PAN looks correct. Authoritative verification confirms whether the PAN is genuinely registered, whether the name matches the government record, and whether the PAN status is active.

According to the Financial Intelligence Unit India (FIU-IND), identity fraud remains one of the top vectors for financial crime reporting in the country, underscoring why surface-level checks are insufficient for regulated entities.

When this verification logic is embedded inside Salesforce, it triggers automatically during lead conversion, account creation, or loan application workflows, not after the fact. Suspicious patterns, mismatches between submitted names and PAN records, or duplicate PAN submissions across multiple accounts become visible before the customer progresses through onboarding.

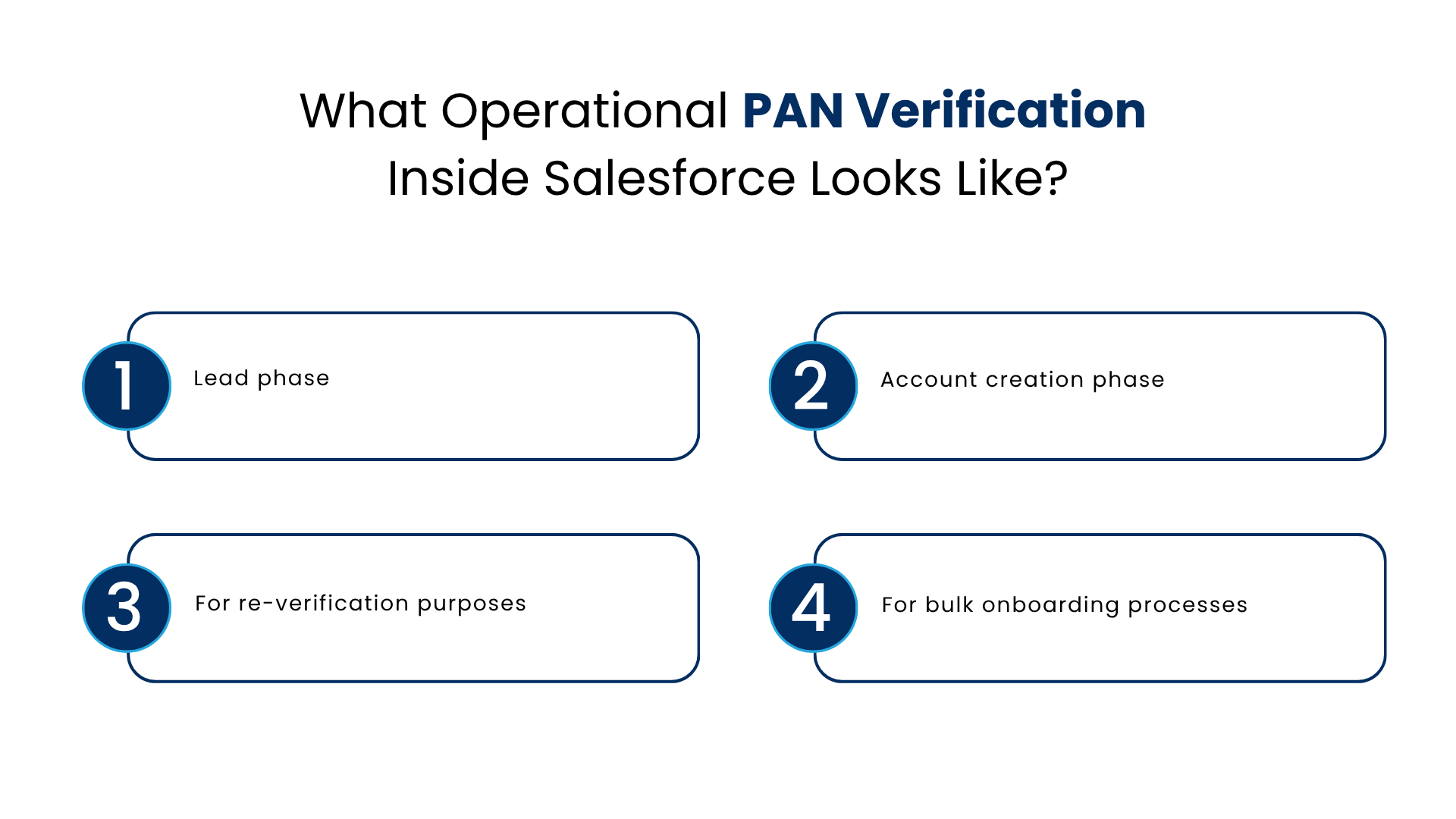

What Operational PAN Verification Inside Salesforce Looks Like?

There’s a meaningful difference between a FinTech that has a PAN verification API and one that has secure identity verification Salesforce workflows embedded in their CRM.

The API-only approach requires a developer touchpoint every time the business wants to adjust verification logic, add a new product line, or update compliance thresholds. It’s inflexible and creates a dependency that slows product velocity.

Properly constructed PAN verification flows based on Salesforce-native design function in a completely different way:

- Lead phase: Whenever a prospective client provides the basic data, which includes their PAN number, Salesforce initiates a verification process by reaching out to the government database. Verification results (verified, name mismatch, invalid/deactivated PAN) appear directly on the record and available to the RM inside the CRM.

- Account creation phase: If the lead gets converted, all the previously mentioned verification result data goes through to the newly created account. No need to repeat the process, as everything has been completed earlier.

- For re-verification purposes: Should a customer’s data be modified at any moment (new address provided, a name changed following marriage, etc.), the software would be able to initiate the process of automatic verification against the latest changes.

- For bulk onboarding processes: Should the company acquire customers as part of a product launch or another marketing campaign, the software can verify the PAN number in bulk batches, with exception records being handled manually.

This is the model that converts Salesforce-based PAN verifications into enterprise-wide capabilities. Salesforce PAN Verification solution leverages exactly such models.

Why FinTech, Banking, and Real Estate All Have a Stake?

The demand for Salesforce PAN verification for Real Estate reflects a broader regulatory trend: PAN-linked compliance is no longer confined to banking and investment products.

Real estate transactions above a certain threshold require PAN disclosure under the Income Tax Act. Developers, brokers, and platform aggregators are increasingly under pressure to verify PAN at the point of buyer registration, not at closing. That requires the verification to happen inside whatever CRM or onboarding platform they use, which in enterprise real estate is frequently Salesforce.

For NBFCs and digital lenders, the pressure is different but equally urgent. Loan origination systems built on Salesforce need PAN verification to integrate with credit bureau pulls, CERSAI checks, and internal fraud scoring models. A fragmented verification approach, where PAN is checked in one system and the credit bureau in another, creates reconciliation delays that add days to loan TAT.

Banking teams dealing with account opening under PMLA guidelines face yet another dimension: the need to verify PAN against the taxpayer database at account opening and then again at certain transaction thresholds. Static onboarding checks aren’t enough; the system needs the ability to re-verify on demand or on trigger.

What unites these sectors is the need for Salesforce PAN authentication that doesn’t degrade into a manual step at the moment it matters most.

Integration with broader KYC and identity verification frameworks such as Manras’s Identryx platform allows PAN verification to function as one layer in a multi-signal identity check. PAN, Aadhaar-based verification, GSTIN validation, and liveness detection can operate in sequence or in parallel, all within Salesforce, without the customer needing to leave the onboarding interface.

According to FATF guidance on digital identity, layered identity verification, combining documentary checks with authoritative database lookups, represents the current standard for effective KYC risk management.

Reducing Manual Dependency Without Losing Control

Another benefit of the Salesforce PAN verification process that needs to be mentioned but tends to go unmentioned is what gets taken out of the equation by such authentication processes.

In human-driven verification procedures, the employees will be getting batches of submitted PANs, checking these PANs using a verification interface, and updating the CRM system accordingly. However, such a procedure has its throughput limit, cannot handle peaks that occur in case of new product launch, leads to errors when the data gets transcribed manually, and makes it impossible to have up-to-date compliance statuses.

Automation takes that manual work out of the process entirely. The question is, though, what happens next? Typically, operations and compliance managers worry about automation because they think it leaves compliance status unverified. The reality, however, is quite the opposite: when the Salesforce CRM is configured properly, automation actually increases visibility since now it becomes possible to focus on exceptions only.

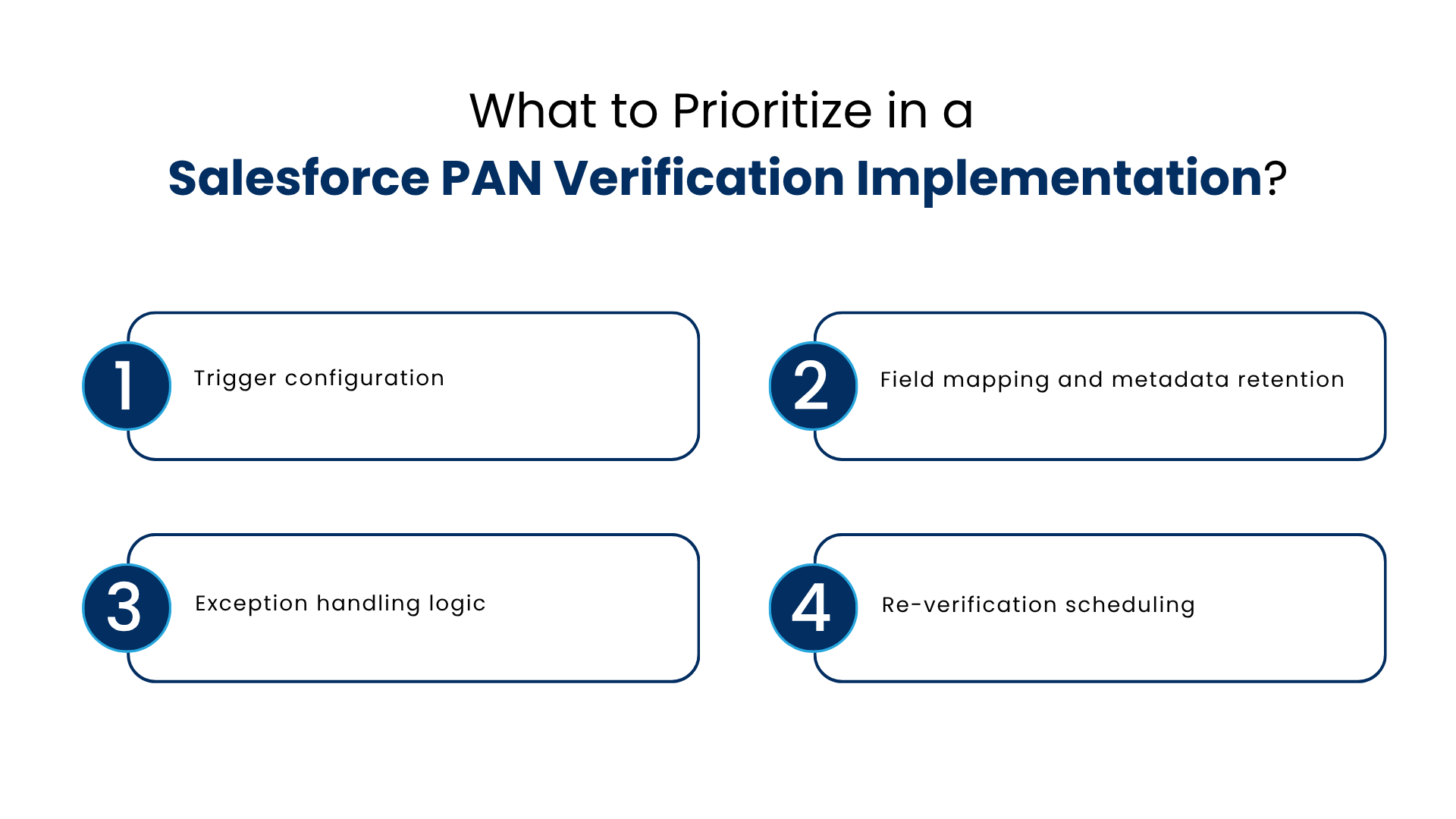

What to Prioritize in a Salesforce PAN Verification Implementation?

For compliance managers, CTOs, and operations heads evaluating this capability, the implementation priorities are consistent across sectors:

- Trigger configuration: Define exactly when verification fires at lead creation, contact update, account conversion, or loan application submission. Over-triggering creates API cost overhead. Under-triggering creates compliance gaps.

- Field mapping and metadata retention: Verification results should be stored with sufficient metadata timestamp, verification source, result code, name match confidence to satisfy audit requirements without requiring a separate evidence management system.

- Exception handling logic: Decide upfront whether failed or flagged verifications pause the workflow entirely, route to a review queue, or allow supervised progression. The right answer depends on the product and risk appetite, but it needs to be a deliberate decision, not a default.

- Re-verification scheduling: For long-lifecycle customer relationships, determine the frequency at which PAN status should be re-confirmed. Tax status can change. PAN deactivations occur. A verification that was valid at onboarding may not remain valid three years later.

Getting these decisions right at the architecture stage is significantly easier than retrofitting them after deployment.

Conclusion

The ultimate value proposition of Salesforce PAN authentication is a resolution of what often feels like a trade-off: speed versus rigor. Fast onboarding and thorough compliance verification are presented as competing objectives. They don’t have to be.

When PAN verification is automated, embedded, and integrated with the broader Salesforce workflow, the compliance check takes seconds rather than hours. The customer experience improves because there are no manual follow-up calls for missing documentation.

The compliance record improves because every verification is logged, timestamped, and auditable. And the operations team improves because their attention goes to genuine exceptions, not routine data processing.

For FinTechs building at scale whether in lending, payments, insurance, or investment this isn’t a feature. It’s an infrastructure requirement.

FAQs

What is Salesforce PAN authentication and how does it work within onboarding?

In simple terms, a Salesforce PAN ID verification solution allows the sales agents to vet and verify every customer within the CRM. The OCR technology fetches the data automatically and matches it with the relevant government records. This helps with faster customer onboarding and reduced verification frauds.

In what way will Salesforce PAN verification minimize the risk of fraud in onboarding customers?

The Salesforce for PAN verification process goes further than just validating the PAN format. It verifies whether the PAN entered is really valid, whether the name matches, and whether the PAN number is still active. It stops fraudulent cases such as synthetic identities, name mismatch, or duplicate accounts from being created in the onboarding process.

What do industries gain the most from Salesforce PAN verification?

Financial services firms, NBFCs, online lending organizations, banking institutions, and real estate portals need to perform PAN verification as part of their process requirements during the initial phase of customer registration. In banking and lending, this is done using the KYC verification, credit bureau, and CERSAI process flows. In real estate, it allows compliance with the Income Tax Act during registration instead of transactions.

Does Salesforce PAN authentication have the ability to verify customer onboarding on a large scale without reducing their productivity?

Yes. The Salesforce PAN validation system can authenticate individual records in real time and perform bulk authentications in situations involving large volumes of customer onboarding. If the record is compliant, it will be cleared automatically, while non-compliant ones will be moved to a queue for further checking.

Why is Salesforce native PAN Verification more advantageous than using a separate tool for PAN verification?

Salesforce native PAN verification ensures that the verification metadata stays in Salesforce’s boundary and can be queried from the Salesforce reports. The separate tool will create a data silo and also requires different audit trail management and cannot be integrated into Salesforce’s approval process and permissions setup.

For more insights, updates, and expert tips, follow us on LinkedIn.